Iron Ore Outlook

Published on - 19th March 2024

Exploring the Future of Iron Ore: A Comprehensive Overview

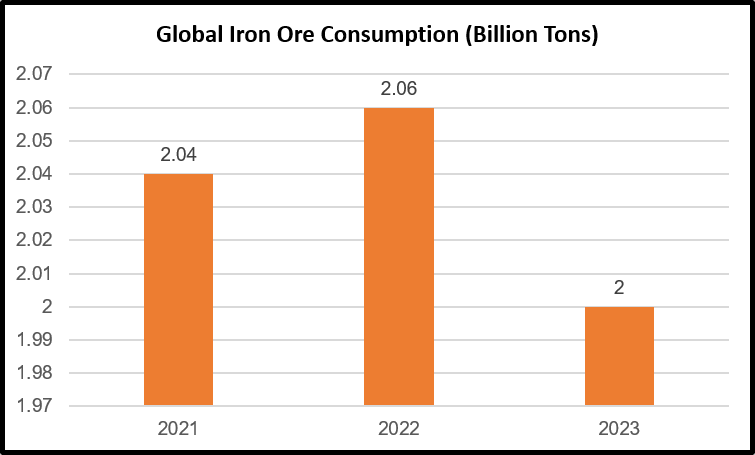

Global demand declined in 2023; weak Chinese demand over property sector woes – Global iron ore demand declined by 2.8% in 2023 to approximately 2 billion tons, with China remaining the largest consumer despite a 1.5% decrease in demand due to reduced domestic steel production amidst a property sector crisis. India, the second-largest consumer, witnessed a 9% increase in iron ore demand during the fiscal year 2023-2024, reaching 228 million tons, driven by growth in the domestic steel sector.

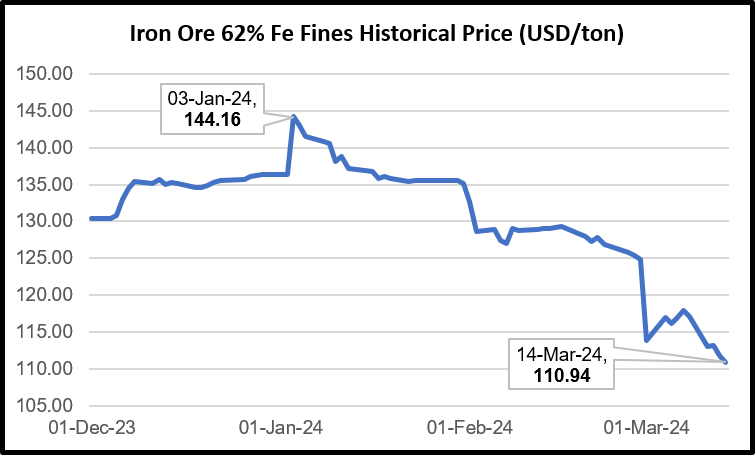

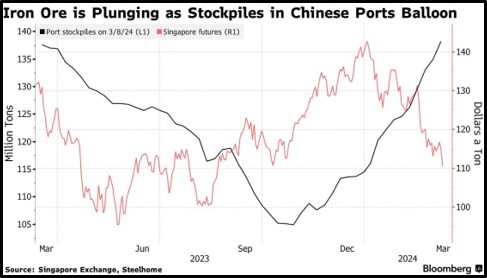

Global demand expected to fall further in 2024; Chinese demand recovery unlikely – Global iron ore demand is expected to decrease in 2024, primarily due to dampened hopes of Chinese demand recovery amidst the ongoing property sector crisis. Iron ore prices have fallen by 25% since the beginning of 2024, reaching a six-month low of $110 per ton, reflecting concerns over reduced Chinese steel demand.

India remains a bright spot for demand outside China – India’s iron ore demand is anticipated to continue increasing in 2024 to meet the rising demand from the domestic steel industry, with projected consumption to grow by 14% in fiscal year 2024-2025. NMDC, a key player catering to India’s iron ore demand, aims to ramp up production to 100 million tons by fiscal year 2030 to address the surge in demand from domestic steelmakers.

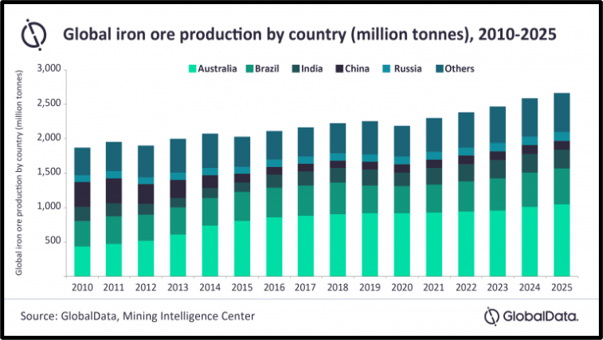

Global supply rose in 2023 driven by increased Australian and Brazilian output – Global iron ore production reached 2.4 billion tons in 2023, marking a 1.1% increase from the previous year, with Australia leading as the largest supplier, producing 960 million tons, and Brazil following closely behind with a supply of 440 million tons, driven by expansion initiatives from key producers like Vale SA.

Global supply expected to surge in 2024 due to new mining projects – Global iron ore production is expected to increase by 3.8% in 2024, reaching 2.6 billion tons, driven by investments in new projects and enhancements in global mining operations. Vale SA, Brazil’s leading iron ore supplier, intends to ramp up production following its strongest December output in five years. Additionally, the launch of projects such as Onslow, Marillana, Western Range, and South Flank is anticipated to bolster Australian iron ore production this year.

Brazilian iron ore supply to rise in 2024 – In 2024, Brazil’s iron ore production is set to increase as Vale aims for an annual output of 320-325 million tons, up from 315 million tons in the previous year. Vale is expanding production capacities at its key mines and plans to establish joint ventures with hubs in the UAE, Saudi Arabia, and Oman to supply iron ore for low-carbon steelmaking, focusing on boosting sales outside of China amid uncertain demand prospects there.

Outlook on Iron Ore – Iron ore prices are poised to decline in the short-to-medium term due to weak Chinese demand and increasing global supply, with port inventories growing globally. Investments in new mining projects and improved operations will further boost supply, including key projects in Australia and capacity expansions in Brazil. Near-term 62% fines iron ore futures are projected at $100 to $115 per ton, while medium-term forecasts suggest a range of $85 to $100 per ton.