Exploring the Future of Aluminum: A Comprehensive Overview

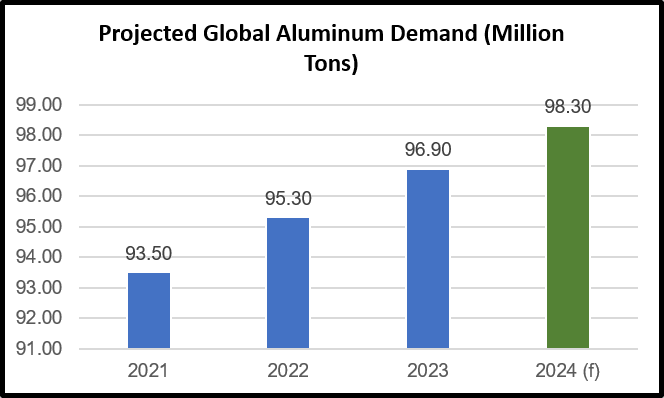

Stable global demand in 2023; Chinese demand key factor – Global aluminum demand grew by 1.7% in 2023 to 96.9 million tons, driven by a 7.6% increase in China’s consumption, mainly from renewables and auto sectors. However, European demand fell by 14% in Q4-2023 due to higher interest rates and energy costs, while North American markets saw a 4.4% decline.

Increased global demand expected in 2024; Chinese demand to slow down – Global aluminum demand is forecasted to grow by 1.4% in 2024 to 98.3 million tons, with China’s growth slowing to 50.4 million tons due to property sector struggles. Recovery in the EU and North America is expected after rate cuts from mid-2024, following a decline in 2023.

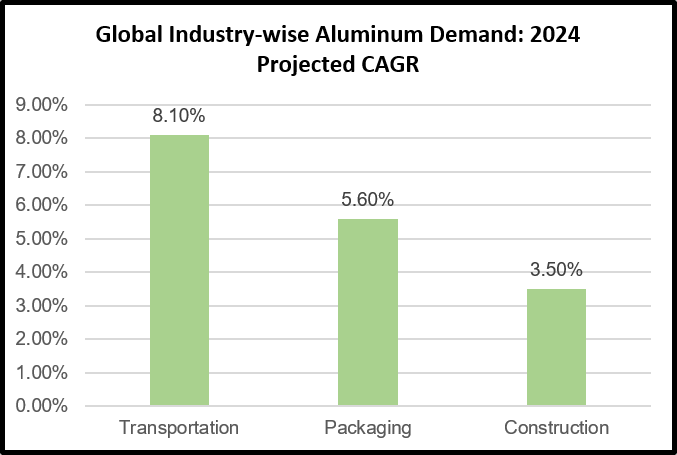

Transportation sector key to global demand growth in 2024 – In 2024, aluminum demand will soar driven by EVs and aluminum replacing plastic and glass in packaging. Transportation demand will grow at 8.1%, while packaging will rise at 5.6%. However, construction demand may slow to 3.5% due to issues in the Chinese property sector.

Transportation sector key to global demand growth in 2024 – In 2024, aluminum demand will soar driven by EVs and aluminum replacing plastic and glass in packaging. Transportation demand will grow at 8.1%, while packaging will rise at 5.6%. However, construction demand may slow to 3.5% due to issues in the Chinese property sector.

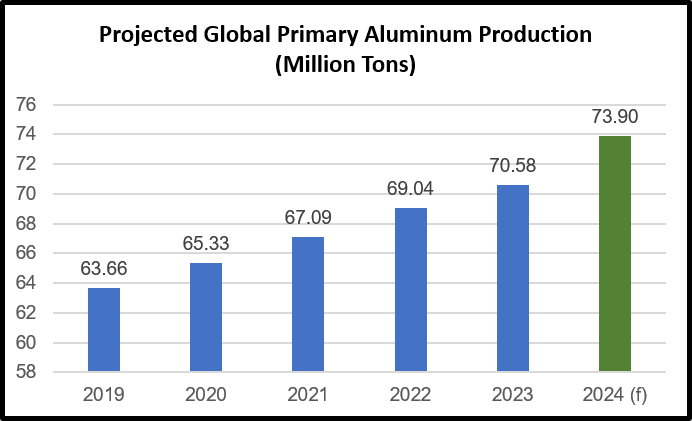

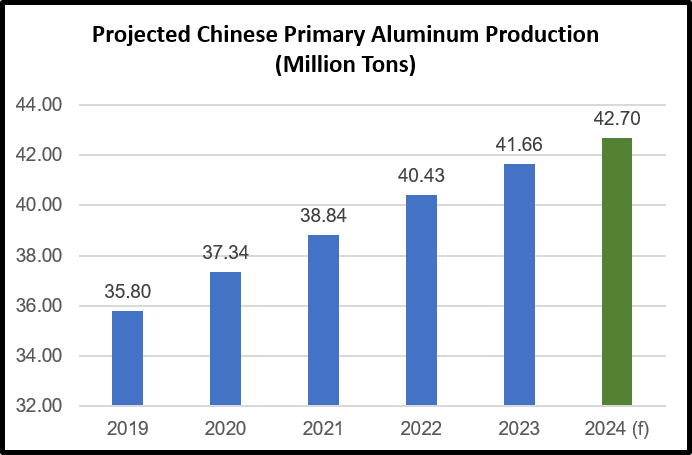

Global aluminum supply expected to surge from H2-2024 – Global primary aluminum supply will rise by 4.7% in 2024 to 73.9 million tons, led by China’s 2.5% increase to 42.7 million tons. New Chinese projects could create surplus. Geopolitical issues may reduce Russian and Eastern European output, but a rebound is possible with lower energy prices. North American output is expected to grow by 3% to 4 million tons, backed by US investments and demand recovery.

Heavily subsidized manufacturing capacities in China raises concerns of global aluminum oversupply – China’s excess manufacturing capacity, notably in steel and aluminum, poses global economic concerns. Subsidized production has led to oversupply in the Chinese aluminum industry, potentially affecting international markets. In response, the US has imposed tariffs on Chinese aluminum imports and introduced tax credits for domestic electric vehicles, limiting Chinese EV access to the US market.

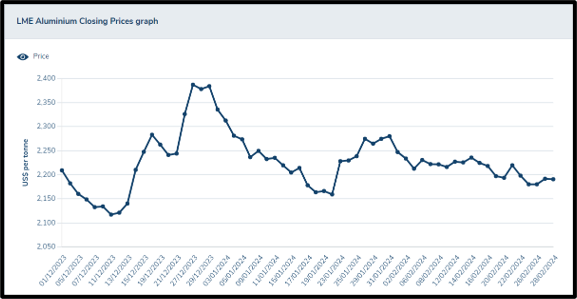

Inventory accumulation in Feb’24 can exert downward pressure on aluminum prices – In February, aluminum inventories surged, with Shanghai reaching a nine-month high of 173,482 tons and LME inventories rebounding to 591,675 tons from a recent low of 525,100 tons. This increase signals a boost in supply levels within the market.

Outlook on Aluminum – Near-term aluminum prices are expected to be bearish due to China’s real estate crisis and global oversupply. US sanctions sparing Russia’s industrial metals have also dimmed hopes for price support. However, a potential price appreciation is likely in the medium term as the market anticipates Fed rate cuts starting from June 2024. Near-term outlook for 3-months LME aluminum: $2,150/ton – $2,300/ton. Medium-term outlook: $2,350/ton – $2,500/ton.

At QuantArt Market Solutions Pvt. Ltd., we prioritize your privacy and aim to provide you with the best browsing experience on our website. By clicking ‘Accept,’ you are consenting to our use of cookies in line with our Privacy Policy. Your agreement acknowledges and complies with our approach to managing data and ensuring your confidentiality. Privacy Policy